4-Point Inspection in San Marcos, CA

San Marcos reads as a new-construction town — the master-planned hillside tracts up toward San Elijo Hills and the build-out around Cal State San Marcos make it feel young. But the older bones are still here: the ranch and split-level homes off Mission Road, the early tracts near Discovery and Richmar, and the 1970s and 80s places that became CSUSM rentals once the campus opened. Those are the homes where a carrier sends a 4-point request before it will write or renew a policy.

I'm Joseph Romeo, and a 4-point inspection is a tight report on the four systems an underwriter actually loses money on — roof, electrical, plumbing, and HVAC. It documents how old each one is, what it's made of, and what shape it's in. It is not a full home inspection and it isn't trying to be. As California's wildfire-pressured carriers pull back from older inland homes, more San Marcos owners — especially landlords renewing on rental stock near the university — are getting asked for one. Below: the scope, the San Marcos-specific reasons it comes up, what I keep finding, how the report works, and where it stops.

Call (619) 752-4399 Schedule an Inspection

Which four systems do I document on a San Marcos home?

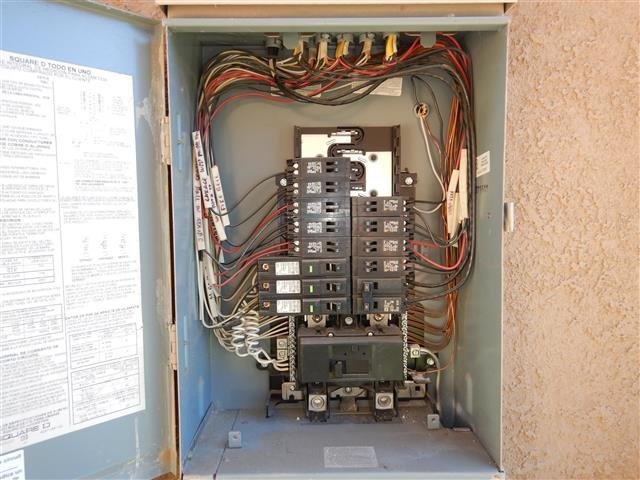

A 4-point is built around four questions an underwriter needs answered, and it leaves the rest of the house alone. I inspect, photograph, and write up the age, material, and condition of each — nothing here pretends to be a buyer's full inspection:

- Roof — covering (composition shingle on the older tracts, concrete tile on the hillside builds), how old it runs, the remaining service life a carrier will underwrite against, and visible trouble like granule loss, slipped tile, or worn flashing.

- Electrical — the panel manufacturer and service amperage, the branch-wiring type, and the conditions insurers decline on: Federal Pacific Stab-Lok, Zinsco, and Sylvania panels, plus knob-and-tube or aluminum branch runs.

- Plumbing — supply material (copper, PEX, galvanized, or polybutylene), drain material, the water heater's age and condition, and any weeping or corrosion at the fittings I can reach.

- HVAC — furnace and air-conditioning type, rough age, and whether it actually runs — which carries real weight here given how hard an inland San Marcos summer leans on a cooling system.

What comes back is a photo-backed summary that drops onto an insurer's 4-point form. Anything concealed or unsafe to reach, I label plainly instead of guessing.

What makes San Marcos 4-points their own animal?

San Marcos splits cleanly between new hillside product and the older flatland and corridor homes — and the things that put a 4-point on the table live in that older half, plus a couple of conditions the terrain itself creates:

- Hillside developments and expansive soil: The clay-heavy soils under much of San Marcos swell and shrink with the seasons, working on slab and supply lines over the decades. A carrier wants the plumbing material and any movement-related leaking on record before it renews an older policy.

- CSUSM rental stock: A lot of the pre-1990 homes near the university got turned into student rentals, where deferred maintenance stacks up — tired water heaters, patched roofs, panels nobody's touched. Landlords renewing coverage on these are squarely in 4-point territory.

- Older corridor housing: The tracts off Mission Road, Richmar, and Discovery predate the master-planned era and sit right in the 25-to-40-plus age band where underwriters stop assuming the roof, panel, and pipes are current.

- Inland heat and wildfire-market pullback: San Marcos summers bake roof coverings and run AC for months, aging both faster than on the coast; combine that with carriers retreating from inland fire-exposed county and the 4-point becomes the screen they lean on hardest.

What keeps turning up on these San Marcos reports?

Because these inspections cluster on the same eras of San Marcos housing, the same findings recur. Knowing them before the policy hangs on it lets you fix or disclose ahead of the underwriter:

- Decline-list panels: Federal Pacific Stab-Lok, Zinsco, and Sylvania panels in homes untouched since the 70s — a frequent reason a policy stalls.

- Aluminum branch wiring: common in a slice of mid-70s San Marcos builds, and a condition carriers ask about by name.

- Aging supply piping: galvanized narrowing with rust in the oldest corridor homes, and polybutylene in certain late-80s tracts — both read as leak liabilities.

- Worn-out water heaters: common in the rental stock — past warranty, corroded, or missing the seismic strapping California requires.

- End-of-life HVAC: condensers and furnaces well past 15 to 20 years, worn down by inland summers and the deferred upkeep typical of rentals.

- Roofs near the edge of insurability: composition shingle thinned by sun, or tile with spent underlayment and flashing even when the tile itself has years left.

I separate a system that's merely old but sound from one a carrier will reject, and I photograph each so the report rests on evidence, not opinion.

How does the visit work, and what does your carrier receive?

It starts with a call to (619) 752-4399 or an email with the address, the home's age, and the carrier or specific form you're satisfying — some insurers want a particular 4-point layout, and knowing it up front saves a return trip. If it's a rental, tell me, and I'll coordinate access with your tenant.

On site I work the four systems directly: open the panel to read manufacturer and amperage, identify supply material at accessible points, check the water heater's age and condition, confirm the HVAC runs, and read the roof for covering, age, and remaining life. It's a focused visit — quicker than a full home inspection because the scope is four systems, not the whole house.

The deliverable is a HomeGauge report documenting each point with photos, the age and material of every system, and condition called out in the plain language an underwriter needs. It usually lands same day or next day, so a renewal deadline or escrow clock doesn't catch you. I report observed condition only — I don't bid or perform repairs, swap a panel, or re-pipe. If a finding needs a specialist, such as a leak pressure-test or a structural opinion, I say so and coordinate or refer the right licensed pro.

Why do San Marcos owners and landlords have me write it?

A 4-point is only as good as the judgment behind what gets flagged. I'm an InterNACHI Certified Professional Inspector (CPI) and I also hold a California CSLB General Contractor license (#1113143). That contractor background is exactly what the four systems demand — I've installed and worked panels, supply lines, water heaters, and roofs, so when I write that a Zinsco panel or a run of galvanized has to go, I know what the fix involves and can tell you straight.

- 20+ years and 10,000+ inspections across San Diego County, from the older Mission Road and Richmar-corridor homes to the San Elijo Hills hillsides and the CSUSM rental pockets.

- 4.9 stars across 106 Google reviews from buyers, sellers, agents, and landlords.

- Independent and conflict-free — I document the four systems for your carrier and don't sell the panel swap, the re-pipe, or the roof, so nothing in the report is steered toward work I'd profit from.

For the panel replacement, re-piping, or roof work the report points to, I coordinate or refer the right licensed contractor rather than pretend the 4-point covers it. I'm InterNACHI CPI and CSLB-licensed; not an ASHI or CREIA member, and I don't post flat prices — the fee depends on the property. Reach me at joe@sandiegohomeinspection.com or the number above.

Which related inspections suit older San Marcos homes?

The 4-point answers your insurer's narrow question. If you're buying, or want a fuller read on an older San Marcos home or a rental you're acquiring, a few companion inspections fold into the same visit:

- Full home inspection — the whole house, structure included, when you need a buyer's-grade report rather than just the carrier's four points.

- Sewer scope — a camera down the main lateral, since the older clay and cast-iron lines under these corridor lots aren't part of a 4-point but fail expensively, and expansive soil doesn't help.

- Roof inspection — a deeper standalone look when the 4-point shows a roof near the end of its remaining life and you need the years detailed.

- Thermal / infrared imaging — for hidden moisture and electrical hot spots the eye misses, useful when the panel or plumbing raises a flag.

- Pool & spa inspection — equipment, bonding, and safety for the backyard pools common on the hillside lots, separate from the insurance four points.

Send me the address, the home's age, and what your carrier is asking for, and I'll tell you which of these genuinely apply before you spend on any of them.

San Marcos 4-Point Inspection FAQs

Why is my insurer requiring a 4-point on my San Marcos home?

Is a 4-point inspection the same as a full home inspection?

I'm a landlord renewing on a CSUSM rental. Can you handle tenant access?

What electrical problems get a San Marcos home declined?

Does San Marcos's expansive soil show up on a 4-point?

How fast can I get the report for my carrier?

Roof, electrical, plumbing and HVAC

Documentation from recent 4-point inspections across San Diego County.

More inspections in San Marcos

- Commercial roof cleaning in San Marcos

- Commercial inspection in San Marcos

- Pool and spa inspection in San Marcos

- Sewer scope inspection in San Marcos

- Home inspection in San Marcos

Nearby and countywide

Were You Happy With Your Inspection?

We are proud of our 4.9-star rating across 100+ Google reviews. If Joseph and the team did right by you, a quick Google review helps other San Diego County buyers and sellers find us.