Roof, electrical, plumbing and HVAC

Documentation from recent 4-point inspections across San Diego County.

4-point insurance inspections in San Diego covering the four major systems insurance companies require: roof, electrical, plumbing, and HVAC. Required by most insurance carriers for homes over 20 years old. Our inspectors are certified and familiar with all major carrier requirements.

Your home deserves the

best inspection

Book today and get a detailed report out to you at light speed.

What Is a 4-Point Inspection?

A 4-point inspection in San Diego County is a focused evaluation of the four systems insurance carriers care about most: the roof, electrical, plumbing, and HVAC. Unlike a full home inspection that documents the whole property, a 4-point report answers one narrow question for an underwriter: are these four systems in serviceable, insurable condition? Carriers typically request one before they will bind a new policy or renew coverage on an older home, and at The Real Estate Inspection Company, owner and lead inspector Joseph Romeo, an InterNACHI Certified Professional Inspector (CPI), performs it to the documentation standard insurers expect.

The name is literal: four points, one purpose. The report records the age, materials, and current condition of each system, flags active defects, and gives the carrier the photographic evidence they need to price your risk.

What's Included

- Roof — covering type, estimated age, remaining service life, and visible damage such as cracked tiles, curling shingles, or failed flashing.

- Roof penetrations and drainage — vents, skylights, and any signs of past or active leakage hidden by our dry climate.

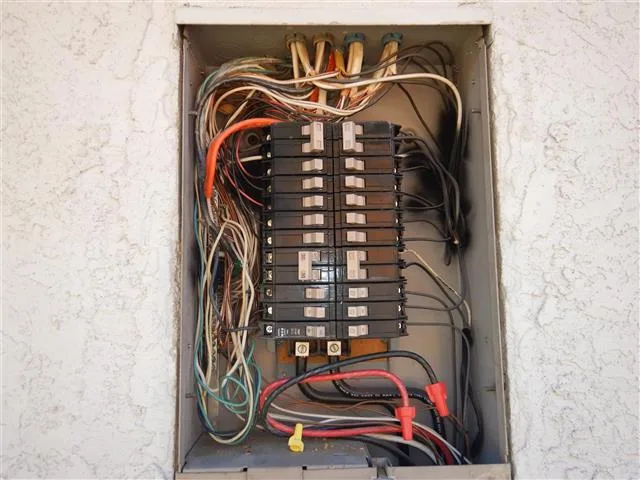

- Electrical panel — brand, amperage, and wiring type, with attention to hazard panels (Federal Pacific, Zinsco) common in older San Diego homes.

- Branch wiring — evidence of knob-and-tube, aluminum, or unpermitted DIY work.

- Plumbing supply lines — material (copper, PEX, galvanized, or polybutylene) and visible corrosion or leaks.

- Water heater — type, age, condition, and proper seismic strapping required in California.

- Drain and sewer indicators — visible signs of aging clay or cast-iron laterals; we can pair this with a camera scope.

- HVAC — heating and cooling equipment age, type, and operational condition.

- Documented photos of each system and every flagged defect, formatted for underwriting review.

Our Process

1. Schedule Around Your Closing or Renewal

Call (619) 752-4399 or request a time online. Tell us whether the inspection is for a new policy on a home you are buying or a renewal on a property you already own, and share your carrier's specific form requirements if you have them.

2. On-Site Evaluation

Joseph Romeo inspects all four systems on site, photographing conditions and defects as he goes. Most 4-point inspections are completed in a single visit; access to the panel, attic, and water heater speeds things up considerably.

3. Same-Day Digital Report

Same-day digital reports are typical. You receive a clean, photo-supported PDF you can forward directly to your insurance agent or underwriter. You can preview our reporting style on our sample reports page.

4. Follow-Up Support

If the carrier asks a follow-up question or needs a defect re-verified after repair, we help you close that loop so coverage isn't delayed.

Who Needs a 4-Point Inspection?

Buyers purchasing a home built roughly 25 years ago or earlier often find their lender's required insurance won't bind until a 4-point clears. Owners renewing a policy may receive a sudden carrier request, especially after switching insurers or when a carrier tightens its underwriting in California's hardening market. Real estate agents use a 4-point to keep an escrow on track when an insurability question surfaces late. And landlords or investors adding an older rental to a portfolio typically need one to secure a new dwelling policy.

4-Point Inspections in San Diego County

San Diego's housing stock and coastal geography create insurability issues you won't see in newer inland markets, and underwriters know it. Older neighborhoods in La Mesa, El Cajon, North Park, and downtown San Diego still have Zinsco and Federal Pacific electrical panels and stretches of galvanized or polybutylene supply piping, all of which carriers treat as elevated risk.

Along the coast in La Jolla, Del Mar, Coronado, and Ocean Beach, salt-air corrosion attacks roof fasteners, flashing, HVAC condenser coils, and water-heater fittings faster than carriers expect, so a roof that looks fine from the curb can hide failing penetrations. Our low-rainfall Mediterranean climate compounds the problem: leaks stay invisible for months because it simply doesn't rain enough to expose them, then a single wet winter reveals years of damage.

Inland, the expansive clay soils of Santee, Escondido, and El Cajon shift with seasonal moisture, stressing slab plumbing and creating the kind of supply-line cracks an underwriter wants documented. Older homes countywide also run aging clay and cast-iron sewer laterals nearing the end of their life. Knowing exactly what each carrier flags in each pocket of the county is the difference between a report that binds coverage and one that triggers more questions.

Pricing & Scheduling

Pricing depends on square footage, the home's age, and access to the panel, attic, and equipment — see our fee schedule for current rates, or request a quote for your specific property. To book, call (619) 752-4399 or email joe@sandiegohomeinspection.com. We schedule across San Diego, Carlsbad, Encinitas, Oceanside, Vista, San Marcos, Chula Vista, Poway, Santee, and surrounding areas, and we coordinate timing around your closing date or renewal deadline.

Frequently Asked Questions

Why do insurers require a 4-point inspection?

Older homes carry more risk in the four systems most likely to cause a major claim — roof, electrical, plumbing, and HVAC. A 4-point gives the underwriter current, photo-documented evidence of those systems so they can decide whether to insure the home and at what premium, rather than relying on the original build date alone.

What's the difference between a 4-point and a full home inspection?

A full buyer's inspection documents the entire property for your decision-making. A 4-point is narrower and written for an insurance carrier, covering only the four systems they underwrite. If you're buying, you often want both.

How old does a home have to be to need one?

It varies by carrier, but requests commonly start once a home is around 25 to 40 years old. Some insurers also require one regardless of age after a coverage lapse or carrier change.

What if a system fails the inspection?

A flagged defect isn't an automatic denial. Carriers usually allow you to repair the issue and submit verification. We document conditions clearly and can re-verify a repaired item so coverage moves forward.

Can you scope the sewer line during the same visit?

Yes. Given San Diego's aging clay and cast-iron laterals, many clients add a sewer camera inspection at the same appointment for a fuller picture of the plumbing.

Systems We Inspect

Examples of the core systems we evaluate during a four-point inspection.